CasinoRank Publishes Insights on Ethiopia’s Online Casino Market

Posted May 20, 2026 by CasinoRank

Ethiopia’s online casino and betting market grew 26.75% YoY despite lacking regulation, CasinoRank reports. The study highlights rapid growth, operator concentration, and rising responsible gambling concerns in an unregulated market.

Ethiopia’s online casino and betting market grew 26.75% year-on-year despite operating without a formal regulatory framework, according to new market intelligence published by CasinoRank. The analysis, which draws on Blask Index data spanning 2022 to May 2026, a trailing twelve-month brand performance dataset covering 148 active operators, and a customer profile survey conducted in April 2026, provides the most detailed publicly available assessment of Ethiopia’s iGaming market to date.

The research tracks a market that surged dramatically through 2025, reaching an all-time Blask Index peak of approximately 25 million in November 2025 before undergoing a sharp correction to around 4 million by January 2026. The market has stabilized near that level since, with current monthly active player sessions of approximately 113,000 and an estimated monthly customer budget of $2.43 million. Over the full trailing 12 months, the combined estimated customer budget stands at $78.8 million, compared with an all-time cumulative figure of $218.81 million across 144 brands.

Brand concentration is high. In January 2026, the top four operators—KonjoBet (26.52%), Chatki (23.83%), Melbet (21.85%), and 1xBet (14.84%)—held more than 87% of measured market share. Over the trailing twelve months, the fastest-growing brands include Melbet (+777.9% YoY), Hulusport (+592.4%), Chatki (+462.3%), and KonjoBet (+426.4%), indicating a market that has undergone rapid structural change over a short period.

The customer profile data reveals a predominantly young, employed, and middle-income player base. The 18–34 age cohort accounts for 65% of players, with 53% employed for wages and 20% self-employed. Annual income clusters in the 20,000–30,000 Ethiopian Birr range, and 50% of players hold a high school education as their highest qualification.

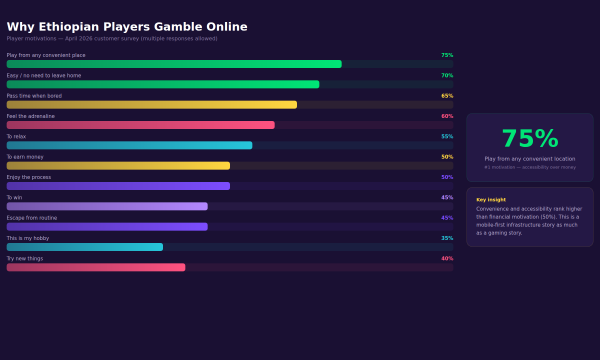

Motivations for play are driven more by convenience than by financial factors. Seventy-five percent of surveyed players cited the ability to play from any location as a primary motivation, with ease of access from home at 70% and entertainment or boredom relief at 65%. Financial motivation—earning money—ranked at 50%. Traditional sports betting is the dominant product at 80% usage, followed by casino games at 60% and slots and instant-win titles, including Aviator, at 50%.

Discovery is led by online search at 70%, display advertising at 65%, and social media platforms, including Facebook, Instagram, TikTok, and Telegram, at 60%. Friend recommendation at 55% represents a significant word-of-mouth multiplier in a market where formal advertising infrastructure is limited.

The responsible gambling data warrants attention. 35% of surveyed players fall into low-risk, moderate-risk, or problem-gambler categories in a market that currently has no formal responsible gambling obligations for operators, no mandated self-exclusion system, and no regulatory oversight of player protection standards.

Samuel O'Reilly, expert at CasinoRank, said the findings point to a market at an inflection point. “Ethiopia has 118 million people, 22 million internet users, and a +26.75% YoY growth rate—but no regulatory framework and no player protection infrastructure. That combination creates both opportunity and risk. The operators who will build durable positions here are the ones who treat responsible gambling and local compliance readiness as strategic priorities rather than afterthoughts,” O'Reilly said.

“The November 2025 spike and the January 2026 correction are a signal, not just a data point. Markets that move that fast in both directions reward operators with local knowledge and patient capital, and punish those treating it as a standard offshore growth play.”

The analysis highlights the absence of a federal licensing framework for online gambling as the defining structural characteristic of the market. Both casino and betting are classified as unregulated, and there is no publicly available regulatory timetable. The research notes that this places Ethiopia in a position comparable to Brazil before its 2023–2024 legislative package—a large, high-growth gray market operating without the institutional infrastructure to manage volatility or player harm systematically.

Seasonality data shows a pronounced second-half-year peak, with activity concentrated from September through December, and November registering the highest monthly index. Weekly and hourly activity is notably uniform, with no significant clustering around weekends or specific times of day. This pattern distinguishes Ethiopian players from those in more mature regulated markets and has direct implications for operator retention and customer service strategies.

The full CasinoRank analysis, including operator rankings and bonus comparisons for the Ethiopian market, is available here.

About CasinoRank

CasinoRank is a global iGaming affiliate brand focused on rating and ranking online gambling platforms. Launched in 2016, CasinoRank operates across multiple verticals, including OnlineCasinoRank, LiveCasinoRank, and BettingRanker.

Get In Touch:

Contact CasinoRank | CasinoRank Facebook

| Contact Email | [email protected] |

| Issued By | Emily Thompson |

| Website | CasinoRank |

| Country | United States |

| Categories | Entertainment , Games |

| Tags | gambling , igaming , casinos |

| Last Updated | May 20, 2026 |